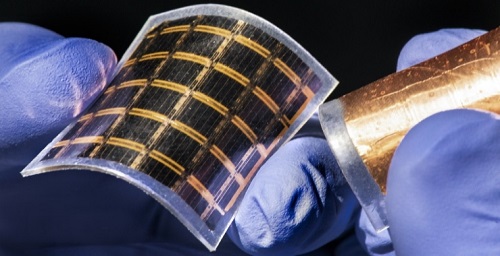

The global ultra-thin solar cells market size is projected to reach USD 178.12 million by 2033, growing at a CAGR of 25.92% during the forecast period, according to a new report by Grand View Research, Inc. The market is driven by increasing demand for lightweight, flexible, high-efficiency photovoltaic solutions across applications such as wearable devices, building-integrated photovoltaics (BIPV), transportation, and remote power systems. Ultra-thin solar cells leveraging materials like perovskites, organic photovoltaics (OPV), and CIGS offer advantages in design flexibility, low material usage, and ease of integration into non-traditional surfaces such as glass, textiles, and curved infrastructure.

The shift toward decentralized clean energy, coupled with rising investments in sustainable architecture and energy-harvesting technologies, is accelerating the deployment of ultra-thin solar technologies. These cells are especially favored when conventional silicon panels are unsuitable due to weight, rigidity, or aesthetic concerns. Innovations in transparent and flexible modules, tandem cell configurations, and roll-to-roll manufacturing enable cost-effective production at scale and enhance energy output under varied light conditions.

Supportive government policies, including tax incentives, renewable energy mandates, and net-zero building codes, further propel market growth. Integrating ultra-thin solar films into windows, facades, and rooftops is becoming a standard energy-efficiency upgrade in the commercial sector. Meanwhile, the consumer electronics industry embraces solar-integrated wearables and self-charging gadgets, aligning with broader sustainability goals and off-grid functionality.

Technological advancements continue to redefine the ultra-thin solar landscape, including improvements in cell durability, power conversion efficiency, and encapsulation techniques to boost outdoor resilience. Researchers are also developing hybrid energy systems that combine solar generation with onboard storage, targeting autonomous operations in IoT devices and EVs. While challenges such as long-term stability and slightly lower efficiency than crystalline panels remain, progress in material science and manufacturing automation is helping mitigate these limitations.

Regionally, Asia Pacific holds the largest share of the global market, driven by robust manufacturing infrastructure, accelerating solar adoption targets, and growing demand for lightweight photovoltaic technologies. China dominates regional production with large-scale investments in perovskite research, roll-to-roll module fabrication, and integration of flexible solar films into consumer electronics and infrastructure. India��s expanding solar capacity, government-led rural electrification schemes, and interest in BIPV contribute significantly to demand. Meanwhile, Japan and South Korea are at the forefront of innovation, focusing on ultra-thin cells for smart buildings, electric vehicles, and IoT-based power systems.

For More Details or Sample Copy please visit link @: Ultra-thin Solar Cells Market Report

Ultra-thin Solar Cells Market Report Highlights

? Based on material, perovskite solar cells dominated the market with a market share of 38.99% in 2024, owing to their exceptional power conversion efficiency, low production costs, and compatibility with flexible substrates. These cells are rapidly being adopted across applications such as building-integrated photovoltaics, wearable electronics, and portable power systems, offering lightweight design and high energy output. Their ability to deliver strong performance under low-light conditions and integrate into compact, curved surfaces makes them the material of choice for next-generation solar technologies.

? Based on end use, the residential segment is anticipated to register the fastest CAGR of 26.89% over the forecast period, driven by the growing adoption of rooftop solar systems and off-grid energy solutions. As homeowners increasingly prioritize sustainable living and energy independence, ultra-thin solar cells offer an attractive solution due to their lightweight design, flexibility, and aesthetic appeal. Advancements in installation ease, declining costs, and supportive government incentives are further accelerating the deployment of ultra-thin solar technologies in residential settings.

? Asia Pacific emerged as the dominant region globally with a revenue share of over 44.46% in 2024. Growth in this region is driven by rapid urbanization, strong government incentives for renewable energy adoption, and expanding solar manufacturing capacities in countries like China, Japan, and South Korea. Additionally, regional players are investing heavily in perovskite and flexible thin-film technologies to support applications in consumer electronics, smart infrastructure, and off-grid energy access across densely populated and remote areas.

? Key industry participants include Oxford PV, First Solar; Hanergy Thin Film Power Group; Ascent Solar Technologies; Heliatek GmbH; Flisom AG; NanoFlex Power Corporation; Alta Devices; Saule Technologies; and Solaronix SA, among others.

Ultra-thin Solar Cells Market Segmentation

Grand View Research has segmented the global ultra-thin solar cells market based on material, end use, and region:

Ultra-thin Solar Cells Material Outlook (Revenue, USD Million, 2021 - 2033)

? Cadmium Telluride

? Copper Indium Gallium Selenide

? Perovskite Solar Cell

? Organic Photovoltaic

? Others

Ultra-thin Solar Cells End Use Outlook (Revenue, USD Million, 2021 - 2033)

? Residential

? Commercial

Research Methodology

We employ a comprehensive and iterative research methodology focused on minimizing deviance in order to provide the most accurate estimates and forecasts possible. We utilize a combination of bottom-up and top-down approaches for segmenting and estimating quantitative aspects of the market. Data is continuously filtered to ensure that only validated and authenticated sources are considered. In addition, data is also mined from a host of reports in our repository, as well as a number of reputed paid databases. Our market estimates and forecasts are derived through simulation models. A unique model is created and customized for each study. Gathered information for market dynamics, technology landscape, application development, and pricing trends are fed into the model and analyzed simultaneously.

About Grand View Research

Grand View Research provides syndicated as well as customized research reports and consulting services on 46 industries across 25 major countries worldwide. This U.S. based market research and consulting company is registered in California and headquartered in San Francisco. Comprising over 425 analysts and consultants, the company adds 1200+ market research reports to its extensive database each year. Supported by an interactive market intelligence platform, the team at Grand View Research guides Fortune 500 companies and prominent academic institutes in comprehending the global and regional business environment and carefully identifying future opportunities.

#UltraThinSolarCells #SolarEnergy #RenewableEnergy #SolarInnovation #ThinFilmSolar #SustainableEnergy #NextGenSolar #SolarPowerSolutions #SolarPanels

Market ScenarioGlobal?Thin Film Solar Cells Market?was valued US$ 16.3 Bn in 2017 and is projected to reach US$ 42.8 Bn by 2026 at a CAGR of 12.8 % during the forecast.Global thin film solar cells market is segmented by product, by end use, and by region.

Reducing renewable tariff subjected to increasing competitive demand may positively influence industry growth.

Increasing electricity demand mainly from rural area among developing countries coupled with regulatory measures toward energy conservation will accelerate the thin film solar cells market.

Reducing renewable tariff subjected to increasing competitive bidding may positively impact market growth.

Middle East & Africa is expected to witness the highest growth rate during forecast, owing to the continual occurrence of solar radiation and high use of renewable energy due to the extensive use of hydropower.Oxford Photovoltaics, Hankey Asia Ltd., Global Solar, Inc., Xunlight Kunshan Co. Ltd., Kaneka Corporation, First Solar, Ascent Solar Technologies Inc., MiaSole Hi-Tech Corp., Trony Solar, and Mitsubishi Electric US, Inc. are major players in thin film solar cell market.Scope of the Global Thin Film Solar Cell MarketGlobal Thin Film Solar Cell Market by Type:? Cadmium Telluride? Copper Indium Gallium Diselenide? Amorphous Thin-film SiliconeGlobal Thin Film Solar Cell Market by End User:? Residential? Commercial? UtilityKey Player analysed in Global Thin Film Solar Cell Market:? Oxford Photovoltaics? Hankey Asia Ltd.? Global Solar, Inc.? Xunlight Kunshan Co. Ltd.? Kaneka Corporation? First Solar? Ascent Solar Technologies Inc.? MiaSole Hi-Tech Corp.? Trony Solar? Mitsubishi Electric US, Inc.? United Solar, Inc.? Solar Frontier K.K.? Solopower Systems? General Electric? Sharp Corporation? XsunX Inc.Browse more detail information about this report visit at:?http://marketgrowthanalysis.com/global-thin-film-solar-cells-marketAbout Us:Market Growth Analysis?is one of the leading digital services provider and a result-oriented company based in Canada.

We are a team of enthusiastic-driven individuals with top notch skills in SEO , Market research.